The Market Power Story

That's a big set of allegations. Everyone knows that the U.S. economy has been looking anemic since the turn of the century, and now a growing chorus of papers by well-respected people is claiming that we've found the culprit. Monopoly power could potentially become Public Enemy #1 for economists, the way taxes and unions were in the 70s, and antitrust could become the new silver bullet policy.

With those kind of stakes, it was inevitable that pushback and skepticism would rev up - after all, you don't just let a big theory like that go unchallenged. My Bloomberg View colleague Tyler Cowen is one of the first to step up to the plate, with a blog post criticizing the De Loecker and Eeckhout paper (BTW I just spelled those both correctly from memory. I want some kind of prize.)

Tyler's post really made me think. It raises some important issues and caveats. But ultimately I don't think it does that much to derail the Market Power Story. Here are some of my my thoughts on Tyler's points.

1. Monopolistic Competition

Tyler:

There are two ways these mark-ups go could up: first there may be more outright monopoly, second there may be more monopolistic competition, with high mark-ups but also high fixed costs, and firms earning close to zero profits....Consider my local Chinese restaurant. Maybe the fixed cost of a restaurant has gone up, due to rising rents and the need to invest in information technology. That can mean higher fixed costs, but still a positive mark-up at the margin.First of all, and most importantly, monopolistic competition is perfectly consistent with the Market Power Story. Monopolistic competition in general does not produce an efficient outcome. Though monopolistic competition doesn't generate long-term profits like monopoly does, it does generate deadweight losses. This is true even when market power comes from product differentiation, as in the typical Dixit-Stiglitz formulation. Monopolistic competition does involve market power, so could also explain the drop in labor share, wages, etc.

So this objection of Tyler's doesn't really go against the Market Power Story, which was always about monopolistic competition rather than outright monopoly.

What about markups vs. profits? In general, Tyler is right - higher markups could indicate higher fixed costs rather than higher profit margins.

But what would these fixed costs be? Tyler suggests rent, but that is a variable cost, not a fixed cost. He also suggests information technology costs -- buying computers for your office, software for the computers, point-of-sale tech, etc. But advances in IT seem just as likely to reduce fixed costs as to raise them. Typewriters cost as much in the 60s as computers do now, but computers can do infinitely more. So much business can be done on the internet, using freely available tools like Google Sheets and Google Docs and free chat apps for workplace communications. Internet outsourcing also dramatically lowers fixed costs by turning them into variable costs.

I'm open to the idea that fixed costs have increased, but I can't easily think of what those fixed costs would be. Maybe modern business organizations are more complex, and therefore require more up-front investment in firm-specific human capital? I'm just hand-waving here.

2. Profits

Tyler:

The authors consider whether fixed costs have risen in section 3.5. They note that measured corporate profits have increased significantly, but do not consider these revisions to the data. Profits haven’t risen by nearly as much as the unmodified TED series might suggest.Tyler is referring to the fact that foreign sales aren't counted when calculating official profit margins, leading these margins to be overstated. Here is Jesse Livermore's corrected series, which uses gross value added in the denominator:

A more accurate measure of true economic profits (i.e., what you'd expect market power to produce) would include opportunity costs (cost of capital) in the numerator. Simcha Barkai does this in a recent paper, also using gross value added in the denominator. Here's his graph for the last 30 years:

His series tells basically the same story as Livermore's - profits have gone up up up. But he doesn't extend back to the 50s, so it's not clear whether higher capital costs back then would reduce the high profit margins seen on Livermore's graph. Interest rates were similar in the 50s and 60s to what they are now, so it seems likely that Barkai's method would also produce a large-ish profit share back then as well.

So it does seem clear that profit has gone way up in recent decades. But a full account should say why profit was also high in the 50s and 60s, and whether this too was caused by market power.

Also, as an interesting side note, Barkai mentions how corporate investment has fallen. That's interesting, because it definitely doesn't square with the "increasing fixed costs" story. Here's Barkai's graph:

If this is a rise in fixed costs we're looking at, where's the investment spending?

3. Market Concentration

Tyler:

In most areas we have more choice, maybe much more choice, than before...ask yourself a simple question — in how many sectors of the American economy do I, as a consumer, feel that concentration has gone up and real choice has gone down? Hospitals, yes. Cable TV? Sort of, but keep in mind that program quality and choice wasn’t available at all not too long ago. What else There are Dollar Stores, Wal-Mart, Amazon, eBay, and used goods on the internet. Government schools. Hospitals. Government. Did I mention government?

Hmm. Autor et al. show that market concentration has increased in basically all broad industrial categories. On one hand, that doesn't take geography and local market power into account - if there's only one store in town, does it matter if it's an indie store or a Wal-Mart? But I think it gives us reliable information that Tyler's anecdotes don't.

Also, Tyler is thinking only of consumer sectors. Much of the economy consists of intermediate goods and services - B2B. These could easily be getting more concentrated, even though we don't come into contact with them very often.

(And one random note: Tyler at one point seems to equate product choice with market concentration, in the case of TV channels. But that's not right. If Netflix is the world's only distribution service, even if it has infinite movies and TV shows, it can jack up the price for watching TV and movies.)

That said, the example of retail is an interesting one. Autor shows that retail concentration has gone up, but I'm sure people now have more choice of retailers than they used to. I think the distinction between national concentration and local concentration probably matters a lot here. And that means maybe it matters for other industries too.

But as for which industries seem more concentrated before, just off the top of my head...let me think. Banks. Airlines (which is why they aren't now all going bankrupt). Pharma. Energy. Consumer nondurables. Food. Semiconductors. Entertainment. Heavy equipment manufacturing. So anecdotally, it does seem like there's a lot of this going on, and it's not just health care and government.

4. Output restriction

Tyler:

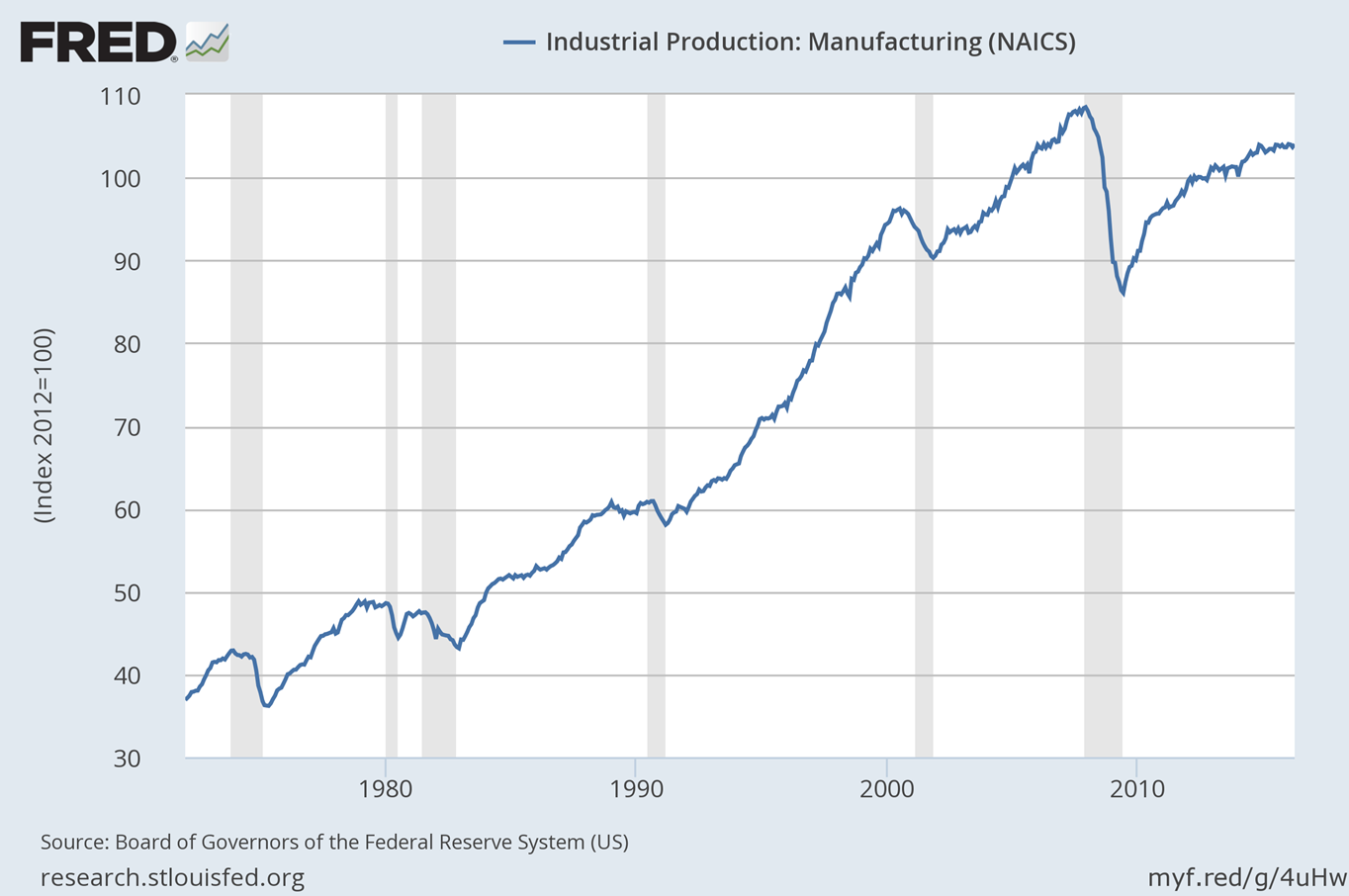

Similarly, the time series for manufacturing output is a pretty straight upward series, especially once you take out the cyclical component. If there is some massive increase in monopoly power, where does the resulting output restriction show up in that data? Once you ask that simple question, the whole story just doesn’t add up.

This is an important point. The basic model of monopoly power is that it restricts output. That's where the deadweight loss comes from (and the same for monopolistic competition too). But overall output is going up in most industries. What gives?

I think the answer is that it's very hard to know a counterfactual. How many more airline tickets would people be buying if the industry had more competition? How much more broadband would we consume? How many more bottles of shampoo would we buy? How many more miles would we drive? It's hard to know these things.

Still, I think this question could and should be addressed with some event studies. Did big mega-mergers change output trends in their industries? That's a research project waiting to be done.

So overall, I think that while Tyler raises some interesting and important points, and provides lots of food for thought, he doesn't really derail the Market Power Story. Even more importantly, that story relies on more than just the De Loecker and Eeckhout paper (and dammit, I had to look up the spelling this time!). The Autor et al. paper is important too. So is the Barkai paper. So are many other very interesting papers by credible economists. So is the body of work showing how antitrust enforcement has weakened in the U.S. To really take down the story, either some common problem will have to be found with all of these papers, or each one (and others to come) will have to be debunked independently, or some compelling alternate explanation will have to be found.

The Market Power Story is still alive, and still worrying.

Update

Forgot to mention this in the original post, but basically I see the case of the Market Power Story - or any big economic story like this - as detective work. We're collecting circumstantial evidence, and while no piece of evidence is a smoking gun, each adds to the overall picture. IF the economy were being throttled by increased market power, we'd expect to see:

1. Increased market concentration (Check! See Autor et al.)

2. Increased markups (Check! See De Loecker and Eeckhout)

3. Increased profits (Check! See Barkai)

4. Decreased investment (Check! See Gutierrez and Philippon)

5. Decreased wages in concentrated markets (Check! See Azar et al.)

6. Increased prices following mergers (Maybe! See Blonigen and Pierce)

7. Weakened antitrust enforcement (Check! See Kwoka)

8. Decreased output (Maybe not? See Ganapati)

So, as I see it, the evidence is piling up from a number of sides here. Economists need to investigate the question of whether output has been restricted. But those who want to come up with an alternate story for the recent changes in industrial organization need one that's consistent with the various facts found by these various sleuthing detectives.

Update 2

Robin Hanson and Karl Smith both have posts responding to De Loecker and Eeckhout's paper and attacking the Market Power Story. Both give reasons why they think rising markups indicate monopolistic competition, rather than entry barriers. But both seem to forget that monopolistic competition causes deadweight loss. Just because it has the word "competition" in it does NOT mean that monopolistic competition is efficient. It is not.

Update 3

Tyler has another post challenging the De Loecker and Eeckhout paper and the Market Power Story in general. His new post makes a variety of largely unconnected points. Briefly...

Tyler on general equilibrium:

If every sector of an economy becomes monopolistic, output will contract in each sector, and it might appear that productivity will decline. But for the most part this output reduction will not be achieved by burning crops in the fields. Rather, less will be produced and factors of production will be freed up for elsewhere. New sectors will arise, and offer goods and services too, perhaps with monopolies as well...

You can cite the deadweight loss of monopoly all you want, but we’re getting more outputs of other stuff. Value-added could be either higher or lower, productivity too.

This seems like a hand-waving argument that economic distortions in one sector are never bad, because they free up resources to be used elsewhere. That's obviously wrong, though. To see this, suppose the government levied a 10000% tax on food. Yes, the labor and capital freed up from the contraction of the food industry would get used elsewhere. NO, overall this outcome would not be good for the economy. Monopoly acts like a tax, so a similar principle applies.

No, resource reallocation does not make market distortions efficient.

Tyler on innovation:

The Schumpeterian tradition, of course, suggested that market power would boost innovation. There are at least two first-order effects pushing in this direction. First, the monopoly has more “free cash” for R&D, and second there is a lower chance of the innovation benefiting competing firms too. I don’t view the “monopoly boosts innovation” hypothesis as confirmed, but it probably has commanded slightly more sympathy from researchers than the opposite point of view. Bell Labs did pretty well.

This is actually a good and important point, and I don't think we can dismiss it at all. There are economists who argue monopoly reduces innovation, and others who argue it increases it.

Tyler on product diversity:

[Y]ou must compare [the efficiency loss from monopolistic competition] to the rise in product diversity that follows from monopolistic competition.

Does market power increase product diversity? That was certainly Edward H. Chamberlin's theory back in the 1930s. When you start getting technical, the question becomes less clear.

Tyler on De Loecker and Eeckhout, again:

But under those same conditions, profits are zero and so the mark-up arguments from the DeLoeker and Eeckhout paper do not apply and indeed cannot hold.

That seems incorrect to me. The fact that long-term profits are zero does NOT make monopolistic competition efficient. So the De Loecker and Eeckhout argument can indeed hold, quite easily. This basic fact - the inefficiency of monopolistic competition in standard theory - keeps coming up again and again. It appears to be a key fact the bloggers now rushing to attack the De Loecker and Eeckhout paper have not yet taken into account.

{kind=link}

Comments

Post a Comment